This piece originally appeared in FIN, James Ledbetter’s fintech newsletter.

In the April 25 edition of FIN, we discussed the conundrum of fintech companies presenting themselves as banks when they aren’t. The federal government is concerned, as FIN described:

There has been a flurry of presumably necessary but somewhat peculiar communications lately from the Federal Deposit Insurance Corporation (FDIC). Reading between the lines of the press releases, it seems like there has been an increase in financial institutions either saying or implying that they are members of the FDIC even if they aren’t. According to the agency, it sent 165 wrist-slapping letters in 2019 and 2020 to institutions it felt were misleading the public.

Lo and behold, this week, a California state regulatory agency slapped down Chime, one of the biggest fintech companies out there, for misrepresenting itself as a bank. The state’s case against Chime seems fairly open-and-shut. The settlement notice states: “Cal. Fin. Code § 561 prohibits any person from transacting ‘business in a way or manner as to lead the public to believe that its business is that of a bank’ without actual authority to engage in such business.”

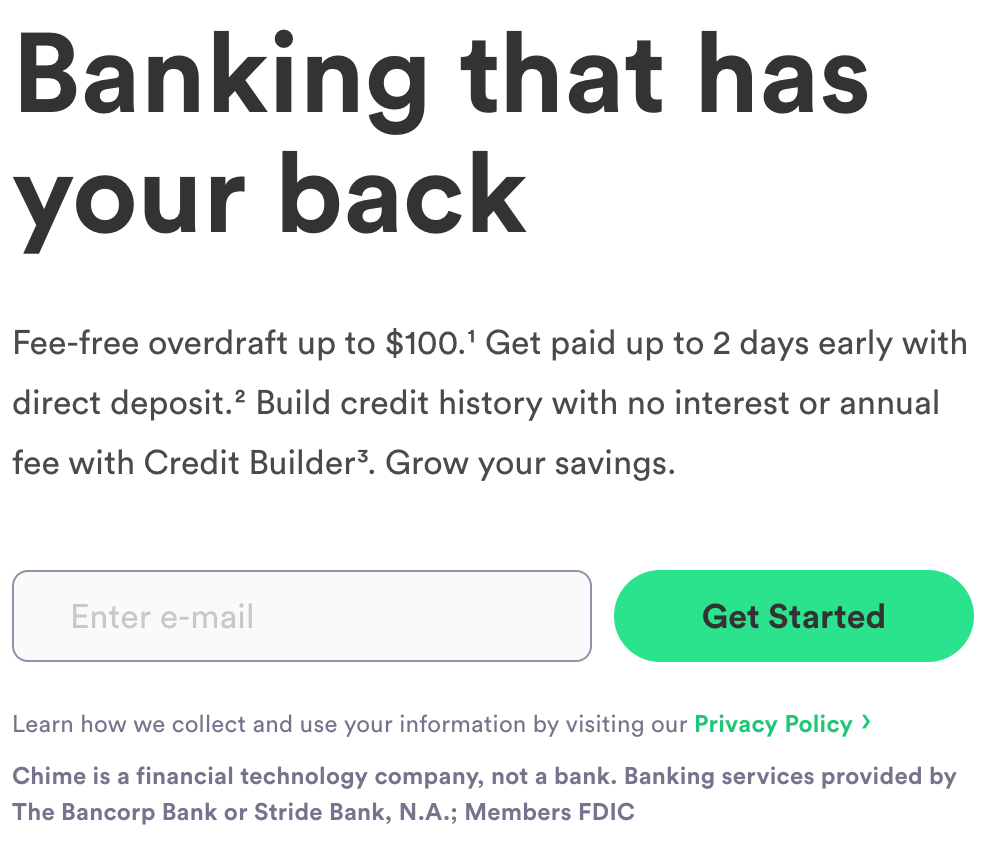

That Chime was implying to consumers that it is a bank it pretty undeniable; the company, for example, used the URL chimebank.com until 2020. Even now, it could be argued that Chime is trying to have it both ways; consider this image from the Chime Web site screenshot on May 7:

The phrase “Chime is a financial technology company, not a bank” is dwarfed by the giant “Banking” headline. Further changes from Chime may be forthcoming. Chime’s rivals were quick to jump on the news. As American Banker reported:

“It’s powerful for us to be able to use the word ‘bank’ in our marketing because we are a legitimate financial institution,” said Dan Henry, CEO of Green Dot, in an earnings call Wednesday. “Words like ‘bank,’ ‘savings account’ and others are things that other neobanks and challenger banks should not be allowed to use.”

The national need to police the definition and activity of banks is pretty fundamental to the very idea of consumer protection. In the US “free banking” system that existed in the early 19th century, bank failures could vary widely from state to state, and the line between poor management, unforeseen circumstances and outright fraud could be impossible to discern. Broadly speaking, giving greater and uniform scrutiny to companies that handle people’s money seems axiomatic. FIN mentioned last week a 2014 speech that a New York regulator gave; it contained the memorable line: “We do not, for example, let someone run a bank out of their garage.”

At the same time, fintech companies can hardly be blamed for responding to market demand created in part by the shrinkage of traditional, FDIC-regulated banks. From 1934 onward, the number of banks and bank branches in the US mostly grew in line with the population. But in 2012, the number of bank branches peaked at 82,965, and has declined every year since; in 2019, the latest year for which the FDIC has records, it was 76,837, and there can be little doubt that the 2020 pandemic took a heavy toll on bank branches.

What might be useful is some way for financial service companies to be accredited and regulated without becoming full-fledged banks (for New Yorkers, think of the distinction between a yellow taxi and a green taxi). The most significant legal distinction between banks and non-banks is the ability to accept and manage deposits. It’s fairly clear from the history of fintech that most startups are not that interested in handling deposits, compared to some of the more lucrative activities that banks engage in (credit and lending). Could there be a government charter that allows fintech companies, under strict scrutiny, to call themselves banks for certain purposes? This week the Federal Reserve said it was considering giving fintech companies greater access to its payment system without needing to establish a relationship with traditional banks; this could be the beginning of rethinking what a bank is and does. While it’s important to enforce the existing laws, it’s equally important to think about ways they might be improved.

Will States Ban Crypto Mining?

California’s decisive action against Chime raises the question of whether individual states are going to set the fintech regulatory agenda ahead of the federal government, even with Biden in office. This week a notoriously tempestuous Brooklyn politician introduced a bill into the New York State Senate that seeks to impose a three-year moratorium on cryptocurrency mining until its environmental impact can be reviewed. The bill notes, reasonably, that the growth of crypto mining challenges the state’s ability to meet its goal of an 85% reduction in greenhouse gas emissions by 2050.

With Democrats now firmly in charge of the New York State legislature, there is more than a trivial chance that this bill, or something similar, could become law. It’s far less clear that the law alone could have the greenhouse gas impact that it seeks. Without a uniform federal policy, crypto miners will simply find other states to do business in. As FIN noted in March, Kentucky is inviting them in with tax incentives.

Rationalizing the Price of Bitcoin

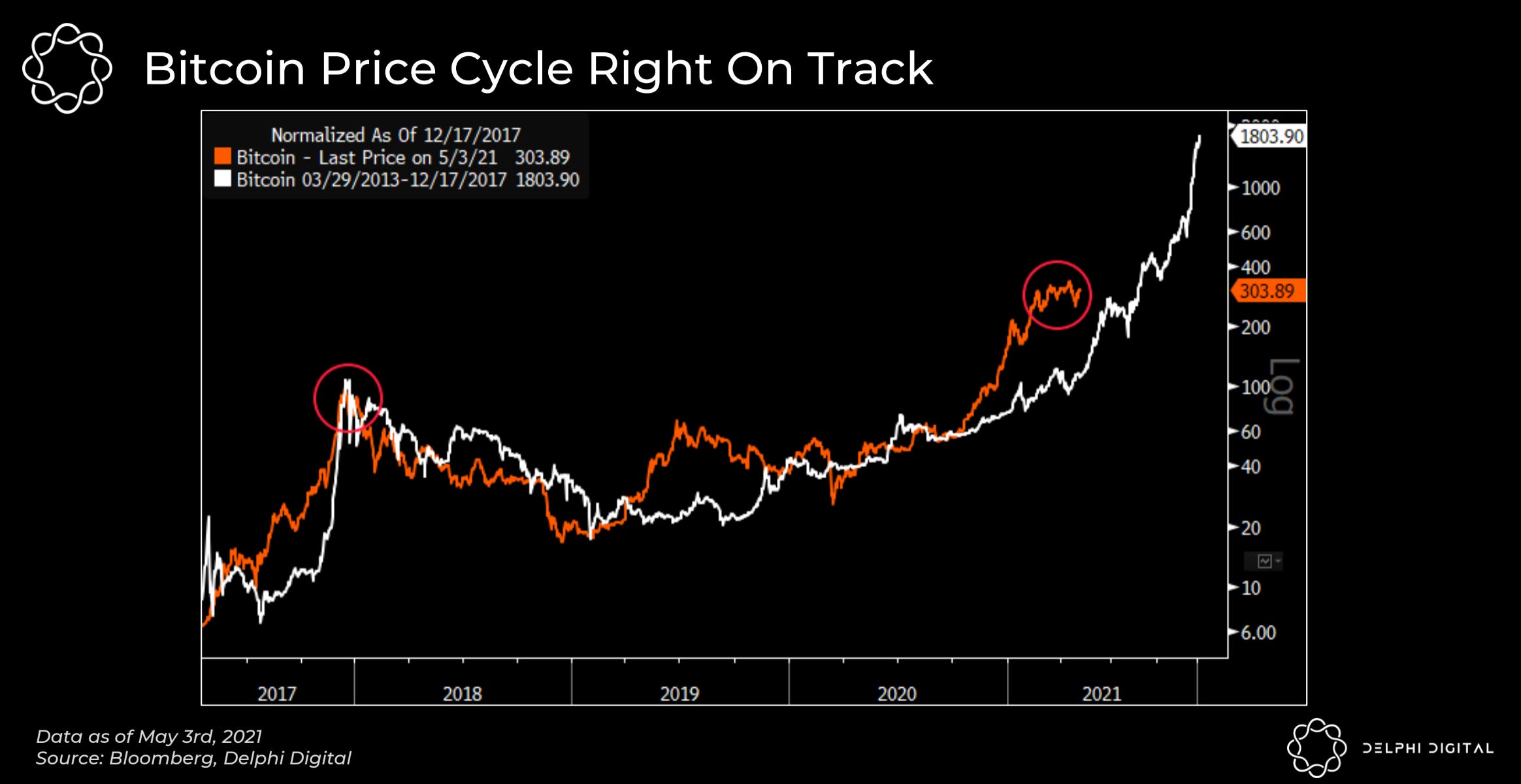

Kevin Kelly, global head of macro strategy at the financial research consulting firm Delphi Digital, gave an intriguing presentation this week at the Bloomberg Wealth Summit. Seeking to strip away explanatory narratives (such as “digital gold” or “disgusting and contrary to the interests of civilization”), Kelly focused instead on Bitcoin’s price history in its decade or so of existence. He found remarkable correspondence between Bitcoin’s current run since late 2020, and Bitcoin’s performance between 2013 and 2017, as demonstrated by this chart:

Kelly’s explanation is a variation on the cycle theory offered by Chris Dixon and Eddy Lazzarin. That is, the price of Bitcoin is one factor in an ecosystem that also includes social media attention, the level of adoption/acceptance of Bitcoin and cryptocurrency, the range of uses of cryptocurrency, and other macroeconomic factors. Assuming this is right, Bitcoin is due for a tumble akin to what happened at the end of 2017—although Kelly was quick to tell FIN “We think this cycle isn’t quite over yet.”

This piece originally appeared in FIN, James Ledbetter’s fintech newsletter. Ledbetter is Chief Content Officer of Clarim Media, which owns Techonomy.