There has been nothing but good news this year on the U.S. economy, which has continued to grow solidly despite the biggest tightening in monetary policy in over 40 years. The Fed funds rate—the overnight interest rate for banks that is the Federal Reserve’s main policy tool—was lifted from zero in March of last year to over 5.25%. Yet that hasn’t hurt the unemployment rate, which remains below 4%, equivalent to full employment.

Recession forecasts—which were nearly unanimous coming into 2023—have been abandoned. Instead, economic activity has accelerated this year. U.S. GDP growth averaged over 2% in the first half, and projections for the third quarter are in the 3-5% range, which would amount to the strongest quarter in almost two years. While prices for many goods and services are higher than they were before COVID-19, the rate of increase—i.e., inflation, which is key to the long-run health and stability of the economy—has fallen dramatically.

While the economy has exhibited surprising strength, financial markets have been rattled over the past couple of months. With the incredible resilience of the economy in mind, Fed policymakers have made it clear that they do not intend to reduce rates anytime soon, and markets have finally given in to that reality. Along with a few other factors outlined below, this has produced a surge in bond yields. Higher bond yields reduce the discounted value of future corporate earnings, and at the same time provide a greater alternative return to equities. As a result, stock prices have declined.

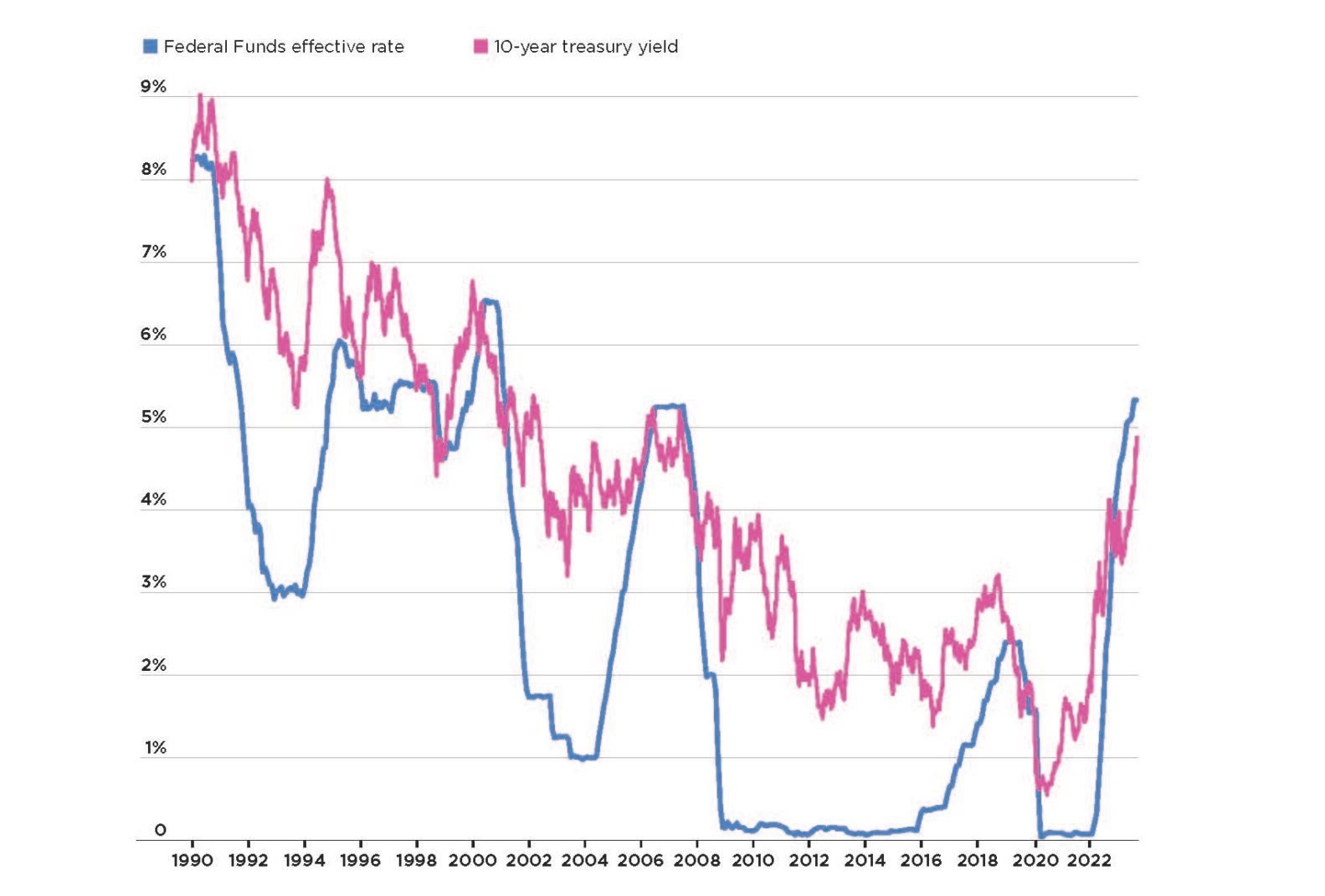

With 10-year U.S. Treasury yields at their highest levels in more than 15 years—over 4.5%—it is reasonable to ask whether they are sustainable. We would argue they are, and that interest rates and Fed policy are returning to levels that were prevalent before the financial crisis.

Bond Yields Over 4% Are Consistent With the Current Environment

Fed policy rates and bond yields have been abnormally low since the financial crisis of 2008. The Fed funds rate averaged less than 1% since then (before the recent Fed tightening), compared with an average of over 4% during the prior 15 years. Policy rates below 1% are not a sign of economic health, as they reflect an economy in need of strong stimulus. Similarly, 10-year U.S. Treasury bond yields averaged around 2.5% after the financial crisis, compared with roughly 5% before.

In addition to the resilient economy allowing policy rates to be higher for longer, federal debt has surged some 40% (by nearly $10 trillion) since COVID-19 appeared. This, in turn, will require the U.S. Treasury to issue more debt, which translates to higher yields to entice investors to buy the additional bonds. Finally, the Fed has shifted from quantitative easing to quantitative tightening: Instead of buying $80bn of U.S. Treasuries and $40bn of mortgage-backed securities per month, it is now allowing $60bn and $35bn respectively of those bond holdings to mature without replacement.

Where Do We Go from Here?

While a recession will occur at some point (the business cycle has not been repealed) it is unlikely to happen anytime soon, barring some exogenous event. The major interest-rate sensitive cyclical sectors—housing and manufacturing—already got clobbered last year in response to the massive tightening in monetary policy and are now bottoming (notwithstanding the recent weakness in housing in response to the jump in mortgage rates).

Meanwhile, the labor market keeps creating jobs, and consumers continue to spend. Household balance sheets remain in very good shape: Debt payments as a percent of disposable income are at reasonable levels, well below what is typically seen prior to recessions. Moreover, consumers retain a huge amount of excess savings (reflecting the COVID stimulus packages as well as reduced spending from when people were stuck at home). Recent estimates suggest around $1.2 trillion.

The U.S. Economy Is Heading into a Fourth Quarter Lull

While a near-term recession seems unlikely, the acceleration in the U.S. economy seen this year is probably over, as there are several headwinds that are slowing things down in the fourth quarter. Student loan repayments resumed October 1. Some 40 million people are saddled with student loan debt amounting to $1.7 trillion, with average monthly payments of $350.

Meanwhile, higher bond yields and lower stock prices will increase borrowing costs and reduce wealth, thus weakening consumer and business spending. Thirty-year mortgage rates are now over 7.5%, the highest in over 20 years. The dollar has risen since mid-summer, which will hurt manufacturing by curtailing exports and increasing imports. Finally, the tightness in the labor market has empowered workers, and worker strikes are increasing.

A government shutdown before yearend remains a distinct possibility, and it would hit the economy hard. Congress extended the September 30 deadline for passing spending bills, but with the House of Representatives in disarray, there is a good chance that it will be unable to come to an agreement that would keep the government running by the end of the year. (The story may be clearer by the time you read this.) That said, spending and output recover once government activities resume and workers receive back pay. As a result, government shutdowns end up having little net effect on the economy.

The U.S. Economy Should Rebound Next Year

Most forecasts for GDP growth in the fourth quarter are in the 1-2% range, and that seems reasonable at this point given these headwinds. What happens next year is more difficult to assess. Most likely the economy will settle into trend-like growth of around 2%, as there are no obvious business cycle triggers to shift growth significantly up or down.

With the labor market and household balance sheets looking healthy and the tightening in monetary policy over for now, a recession next year seems unlikely. At the same time, the effects of higher interest rates on credit and the persistence of a restrictive monetary policy make it unlikely that the economy will go on a tear next year.

There is one factor that could cause the economy to surprise on the upside in 2024: The U.S. is pursuing its first industrial policy in decades. Legislation has been passed that subsidizes infrastructure, semiconductor, and clean energy spending. It is unclear how quickly this will translate into additional capital spending, but it presents a clear upside to U.S. economic growth next year.

Turning to inflation, while the data over the summer showed dramatic improvement, forthcoming figures are likely to show a modest uptick. The Fed focuses on core inflation, which excludes food and energy prices. Core inflation rose at an annual rate close to the Fed’s 2% target over the summer.

A portion of that slowdown, however, was due to temporary effects, such as used car prices coming back down to earth. While falling housing costs are likely to push inflation lower, healthcare and other services are set to exert some upward pressure over the next few months, causing core inflation to move back up somewhat. On a year-over-year basis, core inflation is running around 4%, well above the Fed’s target. Taking all the various factors into account, core inflation is likely to be consistent with a trend of 3-3.5% in the coming months.

What does all this mean for monetary policy? 2023 has turned out better than anyone could have expected when policy rates began to be raised aggressively in March of last year. The Fed has managed to pull off a historic tightening in monetary policy without triggering a recession. At the same time, inflation has come down sharply from its peak of last summer, and the trend has moved closer to the Fed’s target. The tightening of financial market conditions should help keep the brakes on economic growth and moderate inflation.

With the economy, inflation, and financial conditions all falling into place, the Fed is likely to remain on hold for the rest of this year, although there is a chance of one more quarter-point rate hike. The economy is coming off its robust third-quarter pace as yearend approaches, but the odds of a recession anytime soon seem remote. While the sharp drop in inflation seen this summer is unlikely to persist, it should settle at a reasonable underlying pace, albeit somewhat above the Fed’s 2% target. The surge in bond yields and decline in stock prices over the past couple of months seem consistent with the resilience of the economy and the realization that the Fed will maintain a significantly restrictive policy well into next year.

Watch the full video interview below: