This piece originally appeared in FIN, James Ledbetter’s fintech newsletter.

Evidence continues to mount that, in the US, Black consumers and Black-owned businesses use fintech companies disproportionately higher than their overall population numbers would predict. FIN has covered this theme in the past, and yet maintains that this is still not how fintech companies are typically depicted in the mainstream press.

Some background for the most recent data: When COVID-19 first hit the United States in early 2020, the businesses that suffered most were those that are primarily in-person: restaurants, dry cleaners, hotels, transportation, etc. Such businesses are disproportionately owned by women, immigrants and people of color. According to the economist Robert Fairlie, while overall business activity in the US fell by about 20 percent:

African-American businesses were hit especially hard, experiencing a 41 percent drop in business activity. Latinx business owner activity fell by 32 percent, and Asian business owner activity dropped by 26 percent….Immigrant business owners experienced substantial losses in business activity of 36 percent. Female business owners were also disproportionately affected (25 percent drop in business activity).

The Paycheck Protection Program (PPP) was intended to provide relief to struggling businesses. Thus the question of whether, and how, those publicly funded loans (mostly designed to be forgiven) made their way to these highly affected owners is a paramount concern.

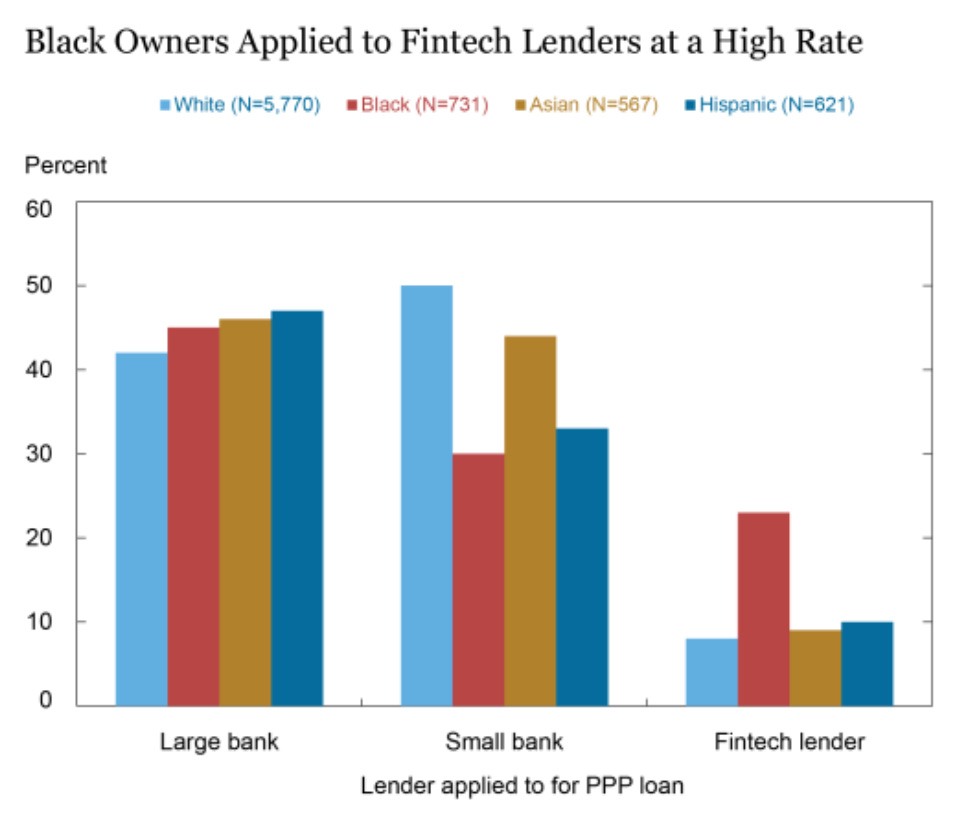

When PPP launched on April 3, 2020, loans were only authorized to pass through banks; a few weeks later, the Small Business Administration authorized nonbanks, including fintech companies, as eligible lenders. This week, the Federal Reserve Bank of New York released a tranche of data and analysis about which American business owners went to which kind of lenders for PPP relief. This chart is illuminating:

Black owners were about as likely to apply through a large bank as anyone else, and far less likely than white or Asian owners to apply through a small bank. But the third category truly stands out: Nearly a quarter of Black PPP applicants went through a fintech lender, well over twice the percentage of other population groups.

The NY Fed notes that only one in three small businesses that applied to a fintech company for a PPP loan had a previous relationship with the lender. Therefore, either a much higher proportion of Black business owners already had fintech relationships, or Black owners were far more willing to experiment with fintech lenders than other owners were.

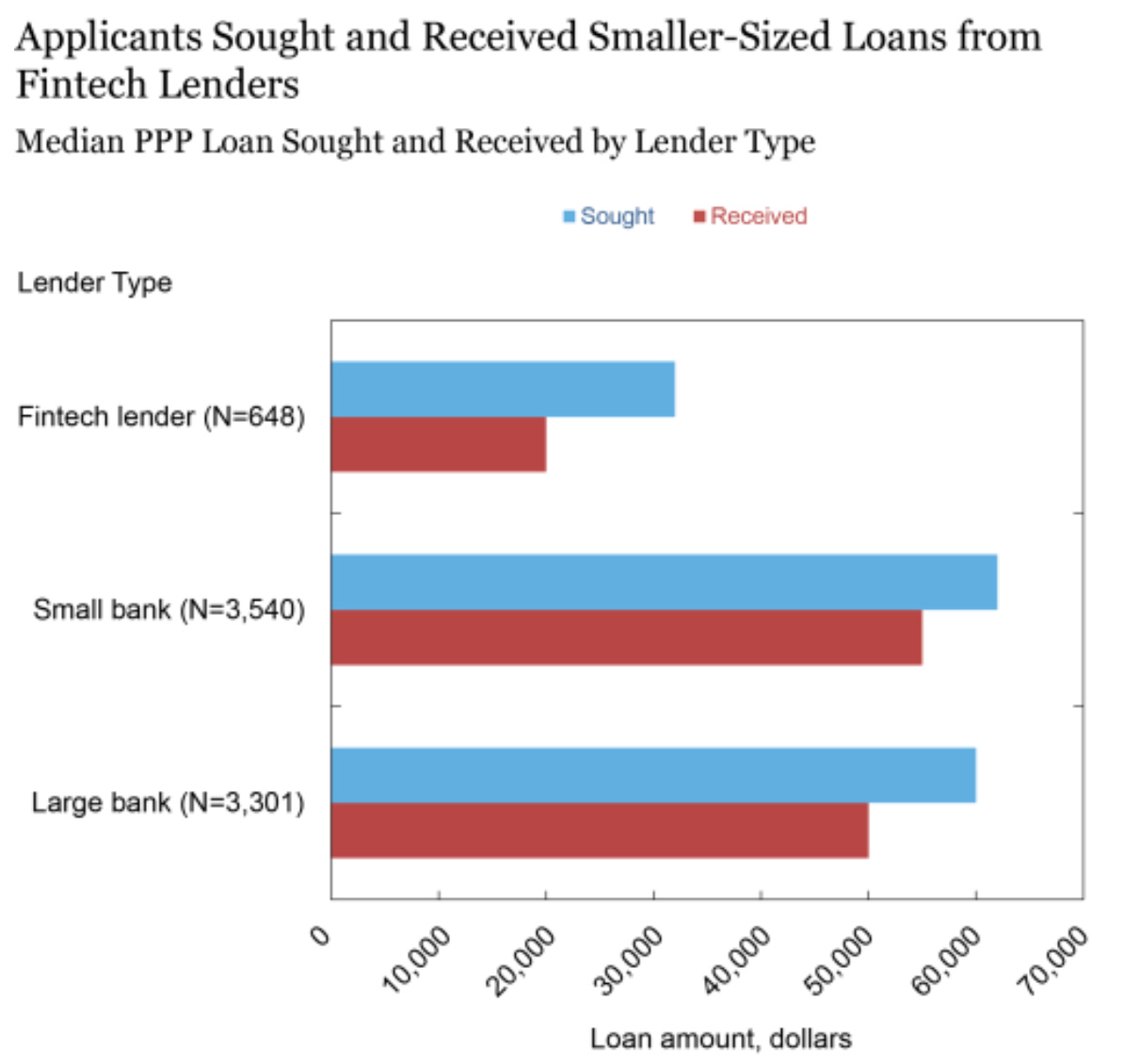

Another notable finding—consistent with much coverage in the past—is that on average, PPP borrowers sought and received PPP loans that were significantly smaller than loans through large and small banks.

This implies that fintech lenders were willing to work with Black business owners over fairly small loan amounts that larger banks wouldn’t bother with because they couldn’t make much money on them.

The NY Fed researchers concluded:

While fintech lenders accounted for a small share of total PPP loan volumes, they played an important role in serving minority owners and businesses that needed small loans but were less likely to receive them from other sources. These smallest of small establishments are critical in supporting vibrant commercial districts and have higher shares of female and minority entrepreneurs. Reflecting this, special efforts were made in the most recent round of PPP funding to make the program more attractive to sole proprietors, independent contractors, and the self-employed.

This is a powerful endorsement of fintech’s impact. America’s racial wealth gap is longstanding and well-documented, and Blacks are the most unbanked and underbanked population in the country. For several decades, America’s banks have paid lip service to the idea of diversity and economic empowerment, even while shutting down branches in minority neighborhoods. When the Federal Deposit Insurance Corporation surveys underbanked Americans about why they don’t have a relationship with a financial institution, the top two reasons are that they can’t afford deposit minimums, or simply “don’t trust banks.” While those may seem like intractable, systemic issues, along comes fintech, demonstrating that in a few short years, some kind of financial relationship is possible. From a business standpoint, the PPP experience represents an opportunity for fintechs to extend their relationship with Black businesses and consumers.

It’s important not to go overboard with this analysis. The PPP is—let’s hope—a oneoff program, and the kind of government support for these loans won’t be available to lenders once it ends. Moreover, not every fintech activity in minority lending is always going to be exemplary.

But the broader question is: Why don’t America’s most prestigious media outlets treat fintech as, at least in part, a diversity success story? Back in December, FIN pointed readers to a detailed McKinsey study showing fintech adoption highest in states with large Black populations, including Georgia, Louisiana and Mississippi. That is not, however, the image we get when reading about fintech in most places.

The Pay-Me-Now Revolution Is Upon Us

One of several lessons taught during the GameStop Götterdämerung is that while a stock trade may appear final because you get a notice within a fraction of a second after you place an order, it (like many other financial transactions) is not actually, officially “settled,” typically for another two days after the notice. The reasons for this “T+2” timeline are regulatory; their desirability is debatable but there is a strong sense that evolving technology and consumer expectations are pushing that settlement time gap ever downward (it used to be 5 days).

This is one reason why some people are excited by blockchain technology, which in theory could bring transaction settlement time very close to zero. In 2019, for example, the Securities and Exchange Commission approved a pilot program run by Paxos to settle equity trades using blockchain. Earlier this month, Bank of America became the largest US bank to participate in this program, alongside Credit Suisse and Nomura.

This week, the custody and clearing firm Apex Fintech Solutions announced that by the end of the third quarter, it intends to be “simulating an instant settlement process.” No, it’s not via blockchain (that will still require change in the law); effectively, Apex will provide a very short-term interest-free loan, giving sellers immediate access to cash worth the transaction price, then settling the transaction the usual way. Still, this is a big deal for at least two reasons: 1) Apex powers stock trades for something like 15 million customers, who use SoFi, Betterment and other Apex customers, and 2) This move will put pressure on other clearing firms to match or beat Apex’s offering.

This piece originally appeared in FIN, James Ledbetter’s fintech newsletter. Ledbetter is Chief Content Officer of Clarim Media, which owns Techonomy.