The United States’ profusion of healthcare facilities, technologies, and therapies are unavailable to most of the world. Yet, for most Americans who need medical care, our country’s unparalleled resources quickly become a curse. It’s no secret that the U.S. healthcare system often leaves its patients with unwieldy out-of-pocket costs. And for those who lack the proper financial funds, these costs can quickly spiral into medical debt. But what is the true extent of medical debt in the U.S.? How does it affect both individuals and communities? And how can those fortunate enough not to suffer from medical debt work to ameliorate the problem for those who do?

The more likely one is to need medical care, the more likely one is to suffer from medical debt. Unlike other kinds of debt, accrued from things like purchasing a house, buying a car, or even going to college, medical debt is not incurred voluntarily. Those in higher income brackets are better able to pay off unexpected bills whereas, for people with limited financial resources, even the smallest, unforeseen medical expense can be unmanageable. Thus, rates of medical debt are at their highest in lower-income zip codes, disproportionately affecting areas that often are already suffering from the brunt of systemic oppression.

The costs of healthcare have skyrocketed over the past fifteen years. According to a 2018 report by the Health Care Cost Institute, the cost of medical care increased by 16 percent from 2012 to 2016—an unduly excessive growth in comparison to the inflation rate of 4.5 percent for the same period. In cities such as New York and Tampa, medical care prices surged by almost 22 percent. In a 2021 annual employer survey, the Henry J. Kaiser Family Foundation (KFF) found that the average annual insurance deductible for single workers is $1,669, four times the average deductible cost in 2006. The combined weight of escalated medical prices and rapidly rising insurance rates have exploded into a debt crisis for everyday Americans.

A study by JAMA, released in 2021 and published by the American Medical Association found that almost 18 percent of Americans owed $140 billion in medical debt to debt collectors—a number that does not include data from the pandemic and is nevertheless almost double the $81 billion that JAMA estimated Americans owed in 2016. Another study done by KFF, investigating different federal data from the 2020 Survey of Income and Program Participation, gauged that Americans owed more than $195 billion in medical debt as of 2019.

One of the most pernicious effects of medical debt is the cyclical nature in which it simultaneously entraps patients while preventing them from receiving the care they need. For fear of being unable to pay for care due to inflated deductibles or other factors, individuals are discouraged from seeking preventative treatments—treatments that could help avert emergency situations. When emergencies do arise, however, this lack of preventative care often snowballs into the extreme costs and ensuing debt that patients were attempting to avoid in the first place. George Halvorson Kaiser Permanente’s former chief executive explained in an investigation done by Kaiser Health News (KHN) that “people are getting bankrupted when they get care, even if they have insurance.”

In addition to deterring people from seeking the care and treatments they need, the U.S. healthcare system also actively denies care to those who have already incurred medical debt. According to KHN’s study, 1 in 7 people with medical debt say that they have been denied access to care because of unpaid bills. The study also revealed that major health systems such as Northwell Health, Trinity Health, Mayo Clinic, and Kaiser Permanente will take legal action against patients who are unable to pay. In fact, Over two-thirds of hospitals have policies that allow them to sue patients or even garnish their wages.

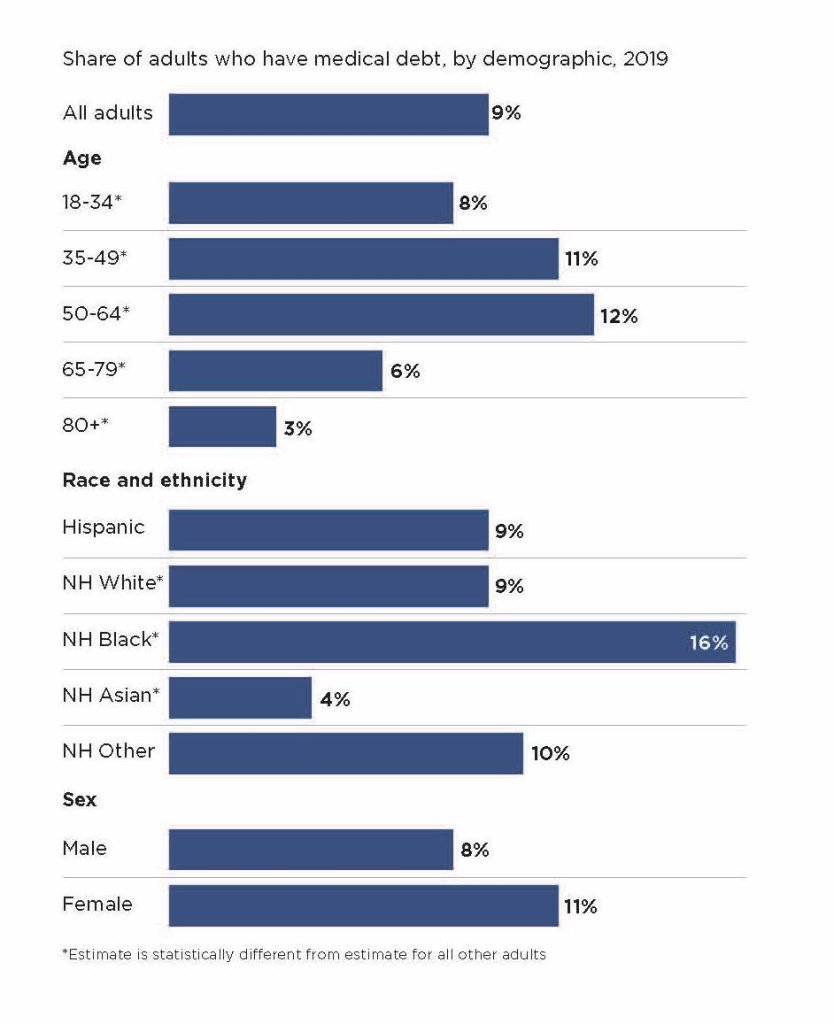

The burden of medical debt is felt not only in the lives of individuals but also across communities, deepening systemic inequalities. According to the KFF analysis, Hispanic adults are 35 percent more likely, and Black adults are 50 percent more likely to struggle with outstanding healthcare costs than white adults. Women also report more medical debt than men due to expenses related to childbirth in combination with lower average incomes. Additionally, adults under the age of 30 are almost twice as likely to suffer from medical debt than those ages 65 and older. In exacerbating and reinforcing longstanding, pervasive social inequalities, medical debt is, at its core, a discriminatory practice.

Despite the insidious nature of medical debt, efforts in the past number of years to curb rates have shown both improvements in healthcare access and economic benefits. The 2013 expansion of Medicaid under the Affordable Care Act proved to be one of the most effective combatants of medical debt in the U.S. In fact, the Medicaid expansion was so effective that as of 2020, rates of medical debt in the eleven states that declined participation were over 30 percent higher than in the states that did participate. As population wellness is a concern closely aligned with the nation’s economic well-being, a KFF investigation of numerous studies found that Medicaid not only benefited patients but also had “overwhelmingly positive effects of expansion on [healthcare] providers.” The same detailed analysis discovered that the financial impact of Medicaid expansion on states additionally had “positive effects, including budget savings, revenue gains, and overall economic growth.”

In addition to the 2013 Medicaid expansion, from startups to nonprofits, there are a number of independent businesses and organizations working to both forgive medical debt and make the process of paying for healthcare more transparent. Ribbon Health, a startup and API data platform, works to aggregate data in order to help patients find high-quality, affordable care. Turquoise Health, a similar venture, has collected over one billion records of pricing data from over 4,000 hospitals. On its website, it also provides an easy and convenient search engine for patients to investigate what costs might look like at their local hospitals. On the nonprofit end, RIP Medical Debt is an impressive 501 charity that simply buys medical debt from the debt collection market and then promptly forgives it. As of August 2022, the group has relieved 3.6 million people of $6.7 billion of medical debt.

The ever-climbing rates of medical debt—that even conservative estimates consider alarming— reveal that the cost of healthcare in the United States is out of control. Despite the evident benefits of debt forgiveness, cost transparency, and expanded Medicaid coverage, the underlying issue of cost remains, leaving the future of medical debt a concerning problem.