Without question, an invitation to join the board of a corporation peopled by friends and colleagues, or a not-for-profit organization with a mission you support, is hard to resist. But before you accept, I caution you to think of being on a board not as a benign hobby-like activity, but as a business deal. In your business, you and your advisors make certain you are protected from exposure to judgments that could result in personal liability. You need to do the same before you join a board.

NOW THE BAD NEWS

If you are a director of a for-profit company, no personal lines underwriting insurance company will offer coverage to protect you from exposure if the firm suffers a devastating judgment and cannot cover the cost. The newsis a bit better if you become a director of a not-for-profit board. For starters, several major carriers offer personal policy coverage for board members of nonprofit entities, condominium associations or cooperative corporations. But this personal policy to supplement the non-profit’s protection has limitations.

First, given the fact that many nonprofits operate with limited budgets, the coverage they secure is often minimal, as little as $1 million for an entire board. But know that the personal policy you rely on to supplement this coverage is limited to bodily injury, property damage and personal injury. Adding to the limitations of the personal policy are some qualifications, specific to the underwriter, regarding any director’s compensation. That means each underwriter’s policy contract must be reviewed.

Think of being on a board not as a benign hobby- like activity, but as a business deal.

The second caution is that personal policy nonprofit director coverages do not provide for fiduciary claims, such as wrongful employment acts or monetary loss from errors or omissions, except in extremely limited situations. Because nonprofit organizations typically can afford only the minimum amount of liability insurance, the limits may be exhausted. If a court-ordered amount exceeds that limit, board members—that is, you—can be personally liable for the judgment amount in excess of the exhausted coverage; that puts your personal assets at risk.

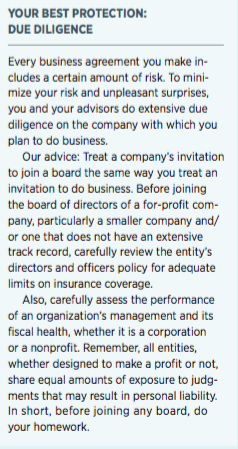

While our firm is working with our underwriters in an effort to address this fiduciary claim void, the developments are severely limited and available only in some states. So, what can you, a well-intentioned individual willing to serve as a board member, do? For starters, read the sidebar on this page, and proceed with caution.

Insurance services provided through NFP Property & Casualty Insurance, Inc., a subsidiary of NFP Corp. Doing business in California as NFP Property & Casualty Insurance Services, Inc. (Calif. License # 0F15715).

This article was originally published in the August/September 2016 issue of Worth.