“The auction room, as anyone knows, is an excellent medium for sustaining fictional price levels, because the public imagines that auction prices are necessarily real prices.”—Robert Hughes, 1984, The New York Review of Books

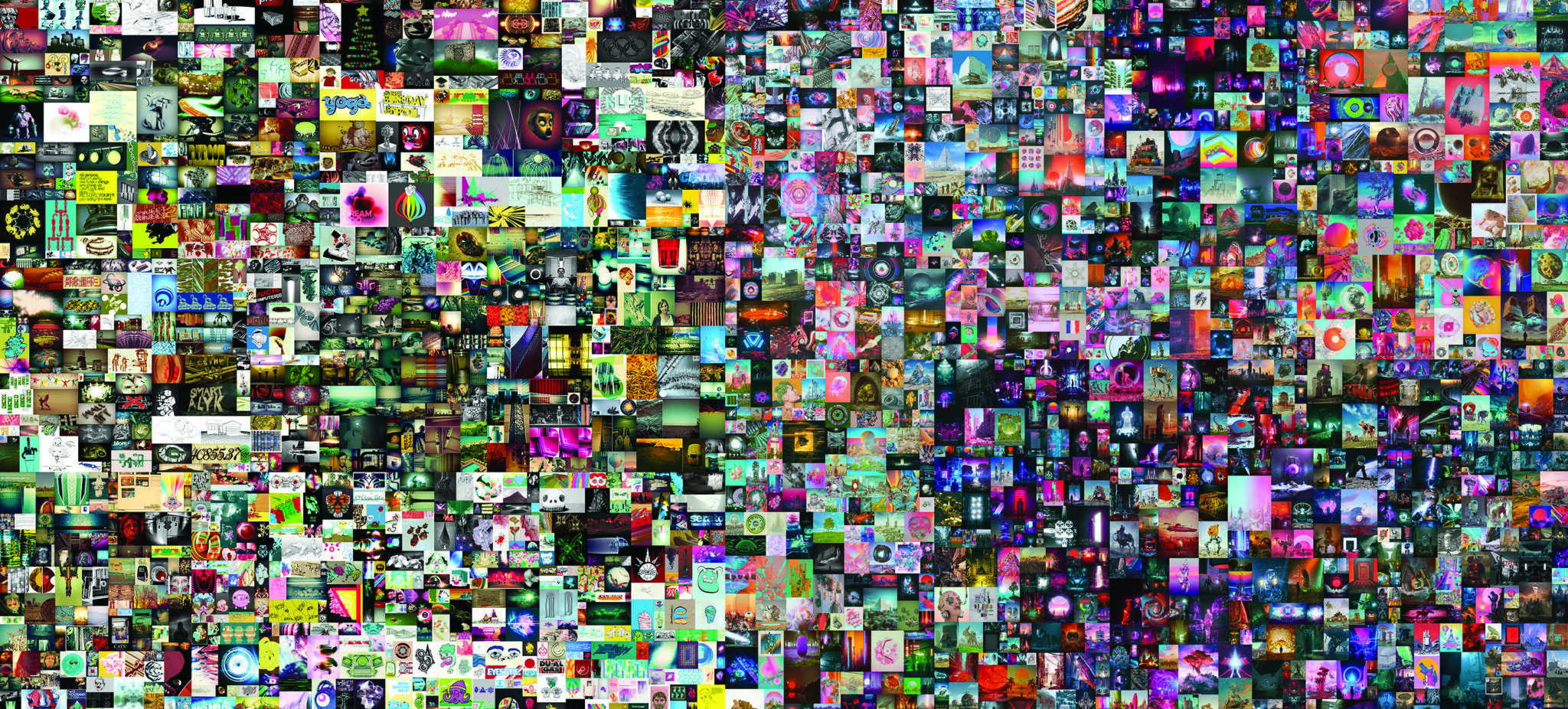

On March 11, 2021, Mike Winkelmann, a digital artist who goes by the online name, Beeple, auctioned off a digital work of art at Christie’s, one of the largest fine-art auction houses in the fine-art world. The title of the work was called, “Everydays: The First 5000 Days,” which was a collage of computer illustrations.

It sold for a staggering $69 million.

Why so much money? It’s a good question that’s difficult to answer. Aesthetically and visually speaking, Beeple’s work isn’t very original or interesting. New York magazine’s art critic, Jerry Saltz tweeted about the work, as well, “I looked up Beeple; just really really derivative Sci-Fi and Conan and Star Wars crapola as far as imagery and imagination go.” That’s not really a vote of confidence. It’s also not that Beeple’s work was the first digital work of art ever made. Digital artwork dates back to the 1990s, even before.

One reason Beeple’s work sold so high was because it included an NFT, or non-fungible token. NFT is an online digital format invented in 2014. An NFT is a digital certificate or digital file that’s connected to a blockchain, basically an online ledger. Blockchain technology also enables cryptocurrencies like Blockchain and Ethereum.

Part of what made the sale so remarkable is that worlds of fine art and digital media always had a frought relationship. This was particularly true when artists or gallery dealers try to sell digital art, which in some cases might be completely digital. Is the artist or gallery selling digital files? Or just the code of a website? And how exactly is it unique?

Nevertheless, in 2021, many inside and outside the fine-art world seemed to be betting on NFTs, and by default, crypto, which is what NFTs are based on. The technology solves these and several other problems associated with digital media, by allowing cryptocurrency to digitally authenticate works bought online. NFTs solves the “unique” problem.

By chance or design or misunderstanding, sale of Beeple’s digital work ushered in a brief golden age of robust buying and selling of NFTs. It was a gold rush, of sorts, to buy NFTs: In December of 2021, Artnews reported that digital artist, Pak, sold a group of NFTs for $91.8 million, which may arguably be the highest price ever paid for a work by a living artist. This past March, the New York Times reported that $44 billion had been spent on NFTs. There was even a new museum dedicated solely to NFTs that opened this past April in Seattle.

Digital art seemed to have come of age with the minting of NFTs.

Then, in May and June of 2022, cryptocurrency prices crashed. The effects of that downturn reverberated in the NFT markets, according to many news outlets. According to Reuters, NFT sales were down sharply in the third quarter of 2022, to $3.4 billion from $12.5 billion at the market’s peak in the first quarter of this year. Bloomberg reported that trading volumes of NFTs are down 97 percent from January of this year, a record high. News outlets also connected the drop in NFT prices to the larger crypto crash. According to Bloomberg, “The fading NFT market is part of a wider, $2 trillion wipeout in the crypto sector.”

But that wasn’t the only bad news NFTs were getting.

In mid-October, Bloomberg published a massive 40,000-word story in Businessweek, written by finance writer, Matt Levine, who attempted to demystify and explain cryptocurrency as well as NFTs. But one might say that both crypto and NFTs got quite a harsh critique in Levine’s story: For example, in the middle of the article, Levine refers to an Esquire article, which discusses how some in crypto are trying to reimagine books as investment opportunities! Levine’s take is this? “The bad way to put this is that every web3 project is simultaneously a Ponzi.”

Levine also questions the thin connection between the code you’re investing in on the blockchain when you buy an NFT and the actual piece of art. He writes, “but what does it mean to say that the NFT is a piece of digital art? The art does not live on the blockchain…. If you buy an NFT, what you own is a notation on the blockchain that says you own a pointer to some web server.” It’s like paying a museum for a Cezanne, and they only give you the page from the museum catalog…or better yet, they’ve only sent you the museum wall label!

On Bloomberg TV, Pat Regnier, Finance editor at Bloomberg Businessweek who edited Levine’s story, said there are other aspects of NFTs to be skeptical about, “I think we’ve all observed that there were enough shenanigans in that [fine-art] market—of creating inflated valuations—[which may give] people a lot of pause about getting into that space.” Perhaps he was referring to Pak or Beeple.

Legally speaking, there are other troubling questions. “The intellectual-property rights to that picture of a monkey,” writes Levine, “are certainly none of the blockchain’s business. It’s not uncommon for the person or company selling the NFT series to 1) own the IP rights to the pictures of the monkeys and 2) promise to transfer those rights, or some of them, to individual holders of the NFTs. But if that happens, it happens off the blockchain; those promises are or aren’t enforceable through the normal legal system.” In effect, buying an NFT might not really solve the problems people expect them to.

For Renier, a rather chilling financial takeaway from Matt Levine’s story is that many within the crypto world have created digital processes and apps that have been repeating the mistakes made in the economic crash of 2008: “People who are building these structures are building things that look a lot like the things in traditional finance that break, and sometimes break disastrously.”

So, NFT investors might want to keep an eye out: It may not just be a very harsh crypto winter that they have to suffer through, but a crypto Armageddon.